Are big banks manipulating the rates of our mortgages? We look at the evidence through the lens of theory.

By Angel Hernando-Veciana

Based on research by Angel Hernando-Veciana and Michael Tröge

Any recent homeowner that has considered a floating rate mortgage has heard of the Euribor or its equivalent LIBOR for currencies outside the Euro zone. These interest rate benchmarks have been so widely used in the last years that their popularity has extended beyond specialists. At some point, it was estimated that the LIBOR was used in contracts with a nominal of $800 trillions: 10 times the annual world GDP! But what is an interest rate benchmark? How is it computed? And why you should worry about it?

My recent work with Michael Tröge studies in detail the process of how interest rate benchmarks are computed and explains why the LIBOR (and similarly the Euribor) may work well when markets are calm but are expected to become unreliable in periods of financial stress like in a financial crisis. We also provide some striking evidence supporting this claim.

But, let’s start with a little bit of history. The LIBOR started back in 1969. At that time, financial markets were not as sophisticated as today, and most of the operations were conducted by banks. In particular, Iran’s Sha needed to borrow such a large amount of money that it was deemed too risky, even by a syndicate of banks. As usual, banks were lending the money long term but they were funding it with their own short-term borrowing. In this occasion, the size of the loan was so big (for the standards at the time) that banks found it hard to bear the risk from a possible spike in the short-term rates at which they were borrowing. A financier, Minos Zombanakis, came with the following idea. What if the interest rate of the loan was variable and correlated with the interest rate at which the banks were borrowing? This is how the LIBOR started, it was the interest rate that was created for this operation. It became so successful that it started to be used in an increasing number of operations. Indeed, when you get a mortgage with a floating interest rate indexed by, say, the Euribor, the bank is doing with you exactly the same as what Minos Zombanakis did with the Sha: transferring the risk of variations in the short-term interest rate to the borrower. And this is why it is so important to have reliable interest rate benchmarks. If they do not work well, agents cannot transfer the risks associated to interest rate variations, and thus there may be a reduction in credit.

Until not so long ago, nobody paid much attention to how the LIBOR or Euribor were computed, and the system seemed to work reasonably well. However, at the onset of the last financial crisis, the Wall Street Journal noted that the LIBOR was moving in a very suspicious manner: at the same time that the risk premium of big banks was increasing, the implicit risk premium in the LIBOR was decreasing. This prompted a sudden interest on the details of the LIBOR’s computation, and what was discovered was very unsettling. The LIBOR was computed as an average of the opinions of the big banks about the rates at which they were able to borrow. It was only that, opinions. They did not need to correspond to real transactions. It was all based on the trust on the honorability of bankers. Certainly, this was not reassuring after the episodes that led to Lehman bankruptcy in 2008.

So, we wondered how such a patchy mechanism had become so successful. To address this question, we proposed a game theory model whose starting point was precisely the fact that the LIBOR was based on an informal survey. This is formalized within the context of “cheap talk” models. These models show that a sender may convey privately known information to a receiver just using “cheap talk messages’’. These are messages for which there is no explicit punishment for providing wrong information, the kind of informal communication at the root of the LIBOR panel. According to this theory, if the incentives of the sender and receiver are closely aligned, even cheap talk communication may be sufficient to convey the sender’s private information. However, this theory also predicts that the less aligned the incentives of the sender and the receiver are, the coarser the maximum information that can be credibly disclosed by the sender.

In our model, the communication from the banks to the LIBOR panel are “cheap talk’’. We exploited the fact that the banks’ individual reports were made public, together with the LIBOR rate. Since the banks were expected to report the interest rate at which they were taking deposits in the interbank market, two types of receivers were reacting to these reports: other banks looking to deposit short term their excess cash (the interbank channel), and traders operating in the stock market that worry about the financial stability of the banks (the stock market channel). The interbank channel arises due to the lack of transparence and centralized operation. Indeed, its analysis hinges on the details of the bargaining and search frictions. For instance, reporting a relatively high interest rate attracts more depositors but this also leads them to demand higher interest rates. We show that under some natural conditions, the interbank channel encourages the bank to report the truth to the LIBOR panel to avoid distortions in its interbank market operations. Our point is that it is the other channel, the stock market channel, that induces the banks to misreport. For instance, in periods of financial stress, like after the collapse of Lehman Brothers, traders in the stock market wonder about the financial stability of the bank, and thus the bank may find it its interest to report relatively low interest rates to convey a solid balance sheet. As the Financial Times put it: “The LIBOR setting process is public and closely watched, so a bank that put in relatively high-rate estimates could spark investor concern about its strength.” (see “Probe Reveals Scale of LIBOR Abuse,” Financial Times, February 9, 2012).

As a consequence, our model predicts that in normal times in which the stock market channel may be less relevant, the interbank channel may be sufficient to ensure the well-functioning of the LIBOR mechanism. However, it also predicts when it may fail: whenever the stock market channel becomes sufficiently strong, like for instance in the aftermath of the 2008 financial crisis. It was precisely then when the Wall Street Journal noted the suspicious behaviour of the LIBOR.

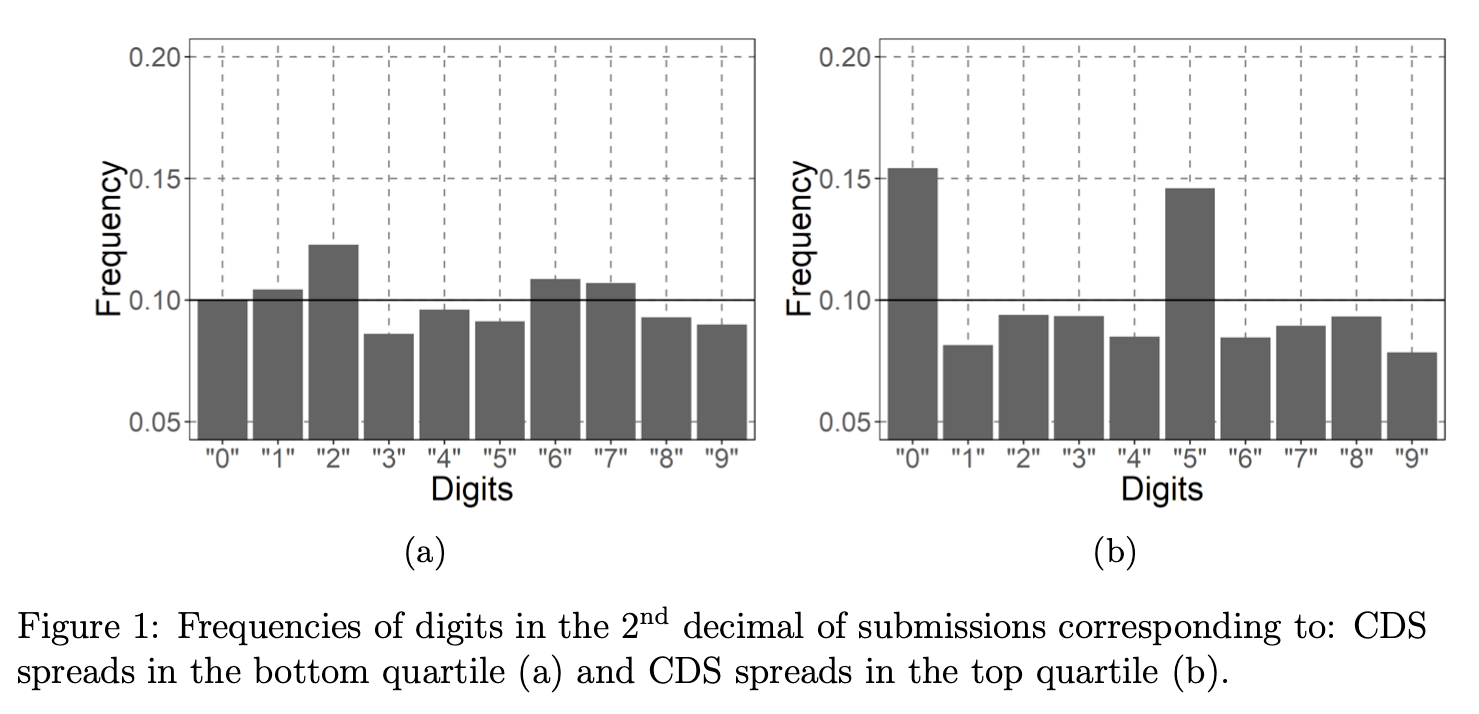

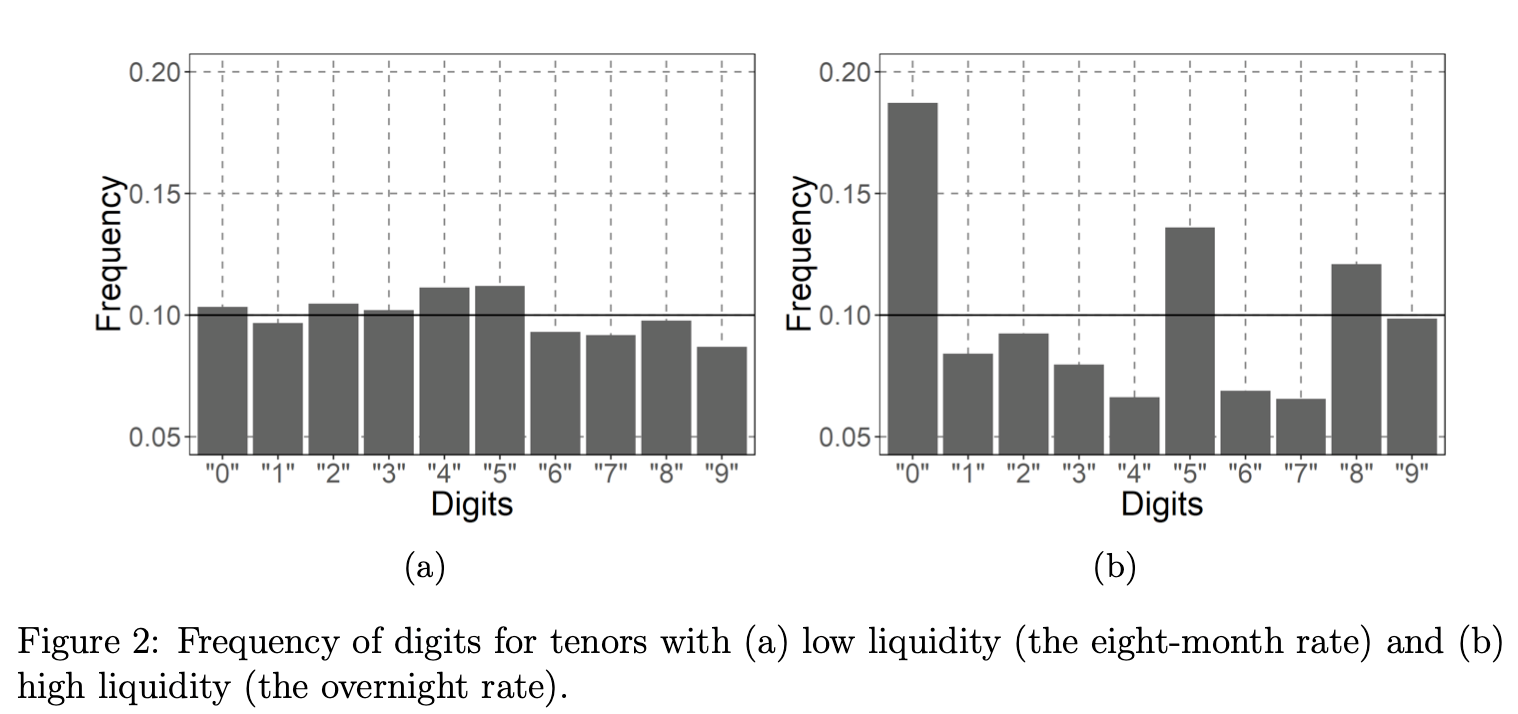

We also explored more in detail the banks’ reports to the LIBOR panel and found some striking patterns that were consistent with our theory but are difficult to explain otherwise. Our theory predicts coarser banks’ reports to the LIBOR panel whenever the stock market effect is stronger and whenever the interbank effect is weaker. As a proxy for the former, we use a high price in the bank’s Credit Default Swaps (CDS), which is a standard measure of the riskiness of an investment. In turn, we use the liquidity of the interbank market to measure the strength of the interbank channel. It is well known that the interbank market for certain maturities, like overnight loans, is more liquid than for others, like 8-month loans. To the extent that more liquid markets are less subject to search frictions, we expect a weaker interbank channel. The next figures provide a very nice summary of our findings.

The two graphs in Figure 1 show that the frequency of zero’s and five’s in the final digit of the reported rates to the LIBOR panel by banks. There is an abnormal number of rounded numbers (i.e., a final digit equal to either 0 or a 5) in periods of financial stress, right panel, but not in normal times, left panel. This is consistent with our theory. In particular, it reflects the relevance of the stock market channel to the extent that more rounded numbers can be identified with coarser communication. Thus, banks seem to be manipulating their quotes in periods of financial stress.

Similarly, the two graphs in Figure 2 show that rounding is a more pervasive phenomena for the more liquid segments of the interbank market, right panel, than in less liquid segments, left panel. Again, this is consistent with our theory and in particular with the relevance of the interbank channel.

Our conclusion is that a surprisingly informal mechanism, like the LIBOR, could work well under some circumstances. However, it is not sufficiently robust to support the multitrillion market that has developed around the LIBOR. More generally, our investigation gives support for the transparency in the construction of financial benchmarks like the LIBOR. Indeed, this is the point we advocated for in a recent editorial we wrote for the Financial Times related to the reform of the LIBOR. Transparency may not only discipline agents, as in our paper, but also provide the means for investigations, like ours, that help us understand the shortcomings of institutions.

Further reading:

Ángel Hernando-Veciana and Michael Tröge (2020), Cheap Talk and Strategic Rounding in LIBOR Submissions, The Review of Financial Studies, Volume 33, Issue 6, June, Pages 2585–2621, https://doi.org/10.1093/rfs/hhz101

Ángel Hernando-Veciana, Michael Tröge (2020) “Libor and Euribor replacements are also vulnerable,” Financial Times, August 4, 2020.

About the authors:

Angel Hernando-Veciana is a microeconomist working in the field of mechanism design and its applications. He is Professor of Economics at Universidad Carlos III.

https://sites.google.com/view/angelhernandoveciana

Michael Tröge is a game theorist working in the field of banking. He is Professor of Finance at ECSP Business School.

https://sites.google.com/view/michaeltroege/