Our research uncovers a new source of earnings inequality: the fact that working hours increase with firm size

Lin Shao, Faisal Sohail and Emircan Yurdagul

Inequality in earnings, which is substantial and growing over time, is of critical concern in economic policy discussions. It is well-known that workers’ employers play a role in the differences in wages across workers. For instance, it is an established fact that larger firms pay higher wages per hour. Our ongoing research uncovers a new source of earnings inequality: the fact that working hours increase with firm size. This amplifies the role of firms in workers’ earnings inequality: workers in larger firms have higher earnings not only because of higher hourly wages, but also because they work longer hours. This article reviews the main facts on the topic and highlights a narrative to reconcile these facts.[1]

Wages increase with firm size

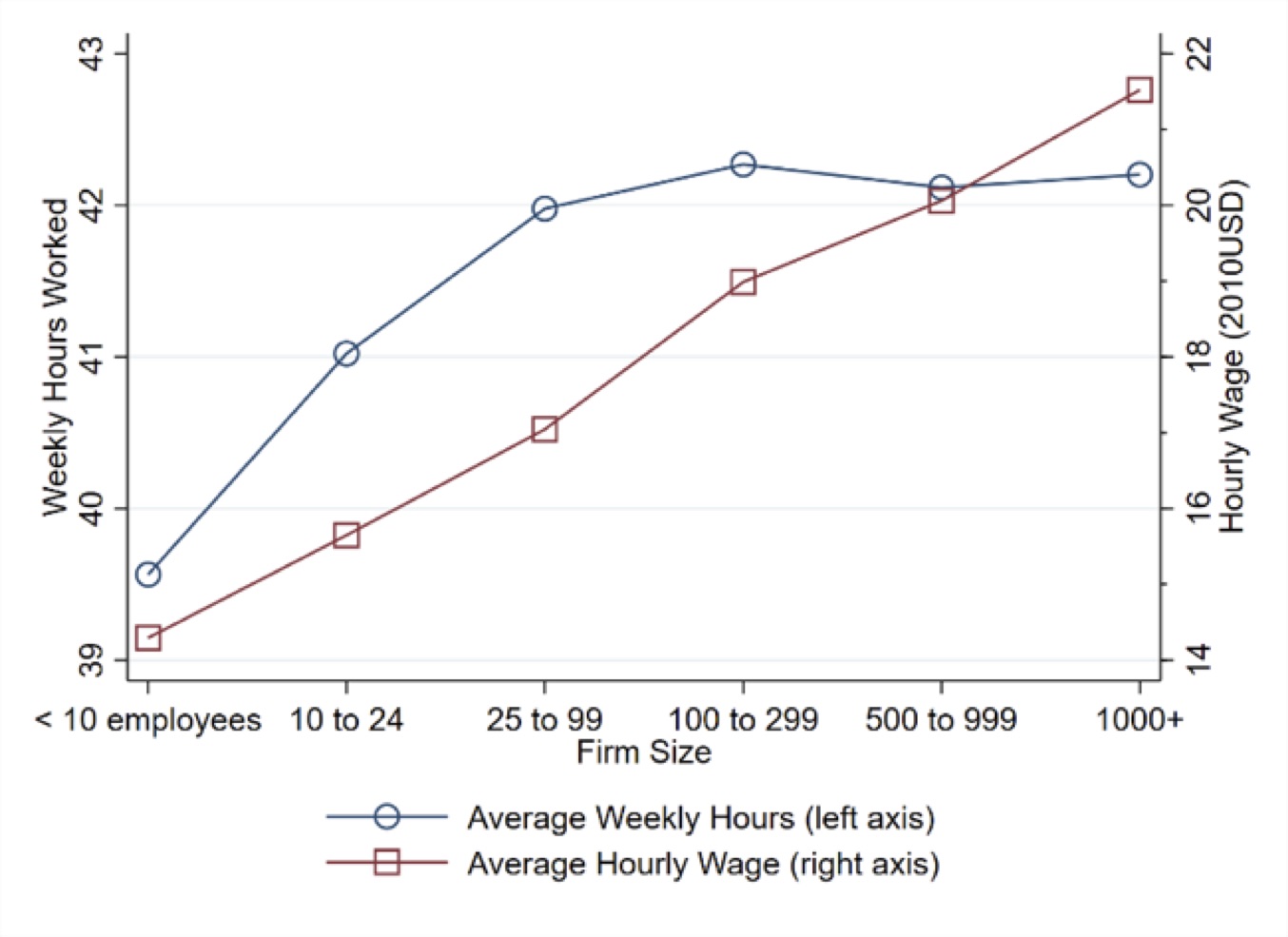

Research on wage inequality reveals that firm size is a key component contributing to wage inequality among workers. Indeed, as shown in Figure 1, there exists a substantial size-wage premium. For example, in 2018, US firms with more than 100 employees pay around 40% higher wages than firms with less than 10 employees. The size-wage premium is present even when conditioning on the characteristics of firms and workers: between two workers in the same state, industry, and with the same observable characteristics (such as age, gender, and education), the worker in the larger firms receive a 23% higher wage than the other worker.[2]

Working hours increase with firm size

What is less known is that these differences appear not only in hourly wages, but also in the number of hours worked in small and large firms. In fact, Figure 1 shows that a worker in a firm with 100-299 employees works about 2.5 hours longer, on average, than a worker in a firm with fewer than 10 employees. This gap persists even when controlling for characteristics of the job, firm, and worker. This difference in weekly hours worked is significant not only statistically but also economically, considering that the difference between the 75th and 25th percentile of hours worked is only about 6 hours in our sample.

Wages depend on hours, differently in small and large firms

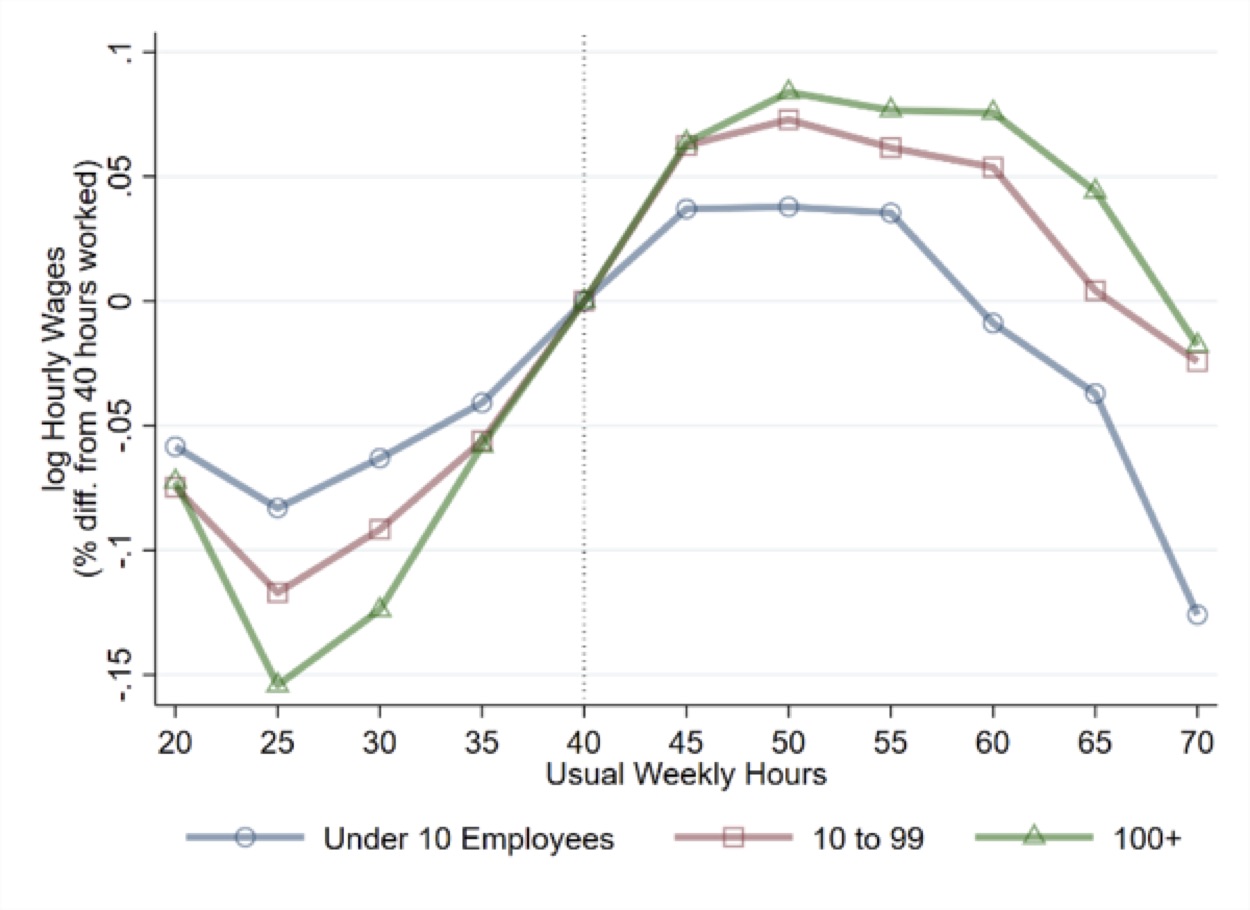

Digging a bit deeper into how wages and hours are determined in firms of varying sizes, it is striking to see that large firms also differ in the way hours and wages relate to each other. Figure 2 shows how wages vary with weekly hours worked by workers’ firm size. In this figure, the first fact that stands out is that wages exhibit “penalties” for working hours that are either too long (say above 60 hours per week) or too short (below 35 hours per week). This fact has been established in previous studies and is robust to controlling for characteristics of workers and firms.[3] A second, novel pattern is that the long-hour penalty is greater in smaller firms, and the short-hour penalty is greater in larger firms.

Why do hours increase with firm size?

How can we reconcile these differences in the hours-wage schedules together with the higher wages and hours worked in larger firms? While all these patterns are interconnected, one possibility is that the size-wage premium is behind both the increasing hours over firm size, and the greater long (short) hours penalties in smaller (larger) firms. Take two workers, A and B. A is willing and able to work longer hours than B—this might be due to, for example, A having fewer domestic duties at home. Suppose that for some reason larger firms pay higher hourly wages than small firms – that is, there is a size-wage premium. Although workers may be considering many different characteristics of these jobs that might push them towards one firm versus the other, worker A has more total income to gain from working in a large firm than B. Hence, all else equal, worker A is more willing to work in a large firm than B due to the size-wage premium. This sorting of long-hour workers, such as worker A, into larger firms, raises the average hours worked in large firms relative to small firms.

Why do wages depend on hours, and what is the role of firm size for this dependence?

Having said this, it may also be that long hours in larger firms lead to the differences between small and large firms in terms of the wage-hours relationships highlighted in Figure 2. To see this, it is useful to discuss first the average pattern in Figure 2, namely, why there might be an inverted-U shape relationship between hours and wages. The answer might lie in complementarities between the working hours of colleagues.

Consider a firm where workers perform tasks that complement each other, such as workers in an assembly line building on each other’s task. Then the workers maximize their productivity if they work similar hours to each other. If a worker shirks and works fewer hours, then another worker will work unaccompanied, reducing their productivity and ultimately earnings. Alternatively, if a worker works much longer hours than others, she herself will be unaccompanied, which again translates into reduced productivity and earnings. An employer could find another worker to fill the voids, but this is subject to costs. All in all, workers are more productive if they coordinate to work a similar level of hours, and they will be penalized for deviating from their colleagues in terms of the working hours. Such “complementarities” between the working hours of workers would explain why we observe the inverted-U shape pattern of wages over working hours.

The next question is, why do long- and short-hour penalties vary by firm size? To understand this, it is crucial to recognize the interaction of differing usual hours across firms and complementarities in production. Since complementarities requires coordination of hours within the firm, earnings penalties are due to workers deviating from a firm’s usual hours. Since the usual hours are longer in larger firms, the penalty for a given level of long hours is smaller in larger firms, and the penalty for a given level of short hours is larger in larger firms. As a result, we would see larger penalties for working shorter hours and smaller penalties for working longer hours in large firms.

Clearly, there is a feedback of wage schedules on working hours of firms of different sizes. Even though the narrative above focuses on rising average hours as the reason for larger penalties for longer (shorter) hours in smaller (larger) firms, such differences in wage-hours menus would, in turn, amplify the positive hours-size relationship since (i) larger firms attract workers with longer desired hours, (ii) the same worker optimally chooses longer hours in larger firms because of differences in earnings penalties.

Implications for welfare

The fact that both wages and hours increase with firm size matters for overall income inequality. A worker in a larger firm will generate a higher income because of the higher hourly wage and because they work longer hours. This exacerbates the differences caused by the wages alone.One question is whether the workers would benefit from a smaller gap in the hours worked between small and large firms. The answer to this is not straightforward. The labor force consists of people who are different in their marital status, number of children to look after, level of wealth, or even their commuting time. These factors all influence the number of hours a worker can/want to work at a given wage. On the one hand, the fact that small and large firms are different in terms of the average hours, hence the wage penalty for long and short hours, gives the workers a more comprehensive menu of hours and wages to choose from. Consider a single parent who needs to look after a child at home and can only work 30 hours a week. The fact that small firms have less severe penalties for short hours, shields this worker against the larger short hour penalties in large firms. On the other hand, it also prevents the single parent from working in a large firm, which on average offers better career prospects. Accordingly, the effects of the patterns in figures 1 and 2 on the welfare of workers are ambiguous and must be carefully evaluated.

About the authors

Lin Shao is a Senior Economist at the Bank of Canada. Her research is focused on macroeconomics, economic development and firm dynamics. http://www.lin-shao.com/

Faisal Sohail is an Assistant Professor at University of Melbourne. His research interests lie within firm dynamics, entrepreneurship, development economics and inequality.

https://sites.google.com/view/faisalsohail/

Emircan Yurdagul is Associate Professor of Economics at Universidad Carlos III. He is a macroeconomist with research interests in firm dynamics, labor economics, economic growth, and international finance.

https://sites.google.com/site/emircanyurdagul/

Further Reading

“Labor Supply and Establishment Size”

References

Bick, Alexander, Adam Blandin, and Richard Rogerson. “Hours and wages.” No. w26722. National Bureau of Economic Research, 2020.

Shao, Lin, Faisal Sohail, and Emircan Yurdagul. “Labor Supply and Establishment Size.” (2021).

Song, J., Price, D. J., Guvenen, F., Bloom, N., & Von Wachter, T. (2019). Firming up inequality. Quarterly Journal of Economics, 134(1), 1–50.

Yurdagul, Emircan. “Production complementarities and flexibility in a model of entrepreneurship.” Journal of Monetary Economics 86 (2017): 36-51.

[1] For instance, in the US, Song et al. (2019) documents a 19 percentage point increase in earnings variance between 1981 and 2013, with two-thirds of this increase attributable to the heterogeneity in workers’ firms

.[2] Unless noted otherwise, the statistics in this article are based on computations in the ongoing work Shao, Sohail and Yurdagul (2021), and correspond to all workers in the US from 1991 to 2018.

[3] See Yurdagul (2017) and Bick, Rogerson and Blandin (2021).