How do family interactions shape housing, caregiving and bequest decisions?

By Matthias Kredler and Daniel Barczyk

Based on research by Daniel Barczyk, Sean Fahle and Matthias Kredler.

Understanding old-age economic behaviour has become increasingly important for public policy and the design of financial products for the elderly. Economists have been making steady progress on it, contributing to the current policy debates. Yet, several features of the data have proven challenging to rationalise in existing theories. In this article, we describe some of these puzzles and explain how our work proposes to solve them. We do so for the case of the U.S., which arguably has the highest-quality data; however, the facts and puzzles we discuss are also present –to a greater or lesser extent– in other rich countries.

Start with the so-called retirement savings puzzle. The elderly in the U.S. de-cumulate their wealth relatively slowly and leave sizeable bequests. A closely related observation is that most elderly own their homes and are reluctant to sell them unless they move into a nursing facility or are confronted with the death of their spouse. Through the lens of standard economic theory, this constitutes a puzzle. Why is so much wealth tied up in an illiquid asset, which instead could be used for consumption when renting a smaller-sized home? One prominent explanation for the puzzle is the altruistic bequest motive: If parents derive value from leaving wealth to their children, maintaining wealth (also in the form of housing) seems sensible. While the existence of altruism among biologically related family members is hard to dispute, economists are interested in whether altruism provides a quantitatively credible explanation – a question that has remained elusive.

A second fact casts doubt on altruism being the central explanation for the retirement savings puzzle: Bequests and savings behaviour of the elderly without children closely resembles that of elderly parents. However, we point out that one important implication of altruism has so far been overlooked: The presence of children not only entails altruistic bequests but also better insurance for parents. This is so because the elderly face large uninsured risks from long-term care. Nursing homes are costly, especially in the U.S. Being a parent mitigates expenditure risk since children often provide informal care to their parents at home. In other words, we argue that while altruism alone increases parents’ bequests, the lower need for precautionary savings counteracts this force and can explain the puzzling similarity between parents and the childless.

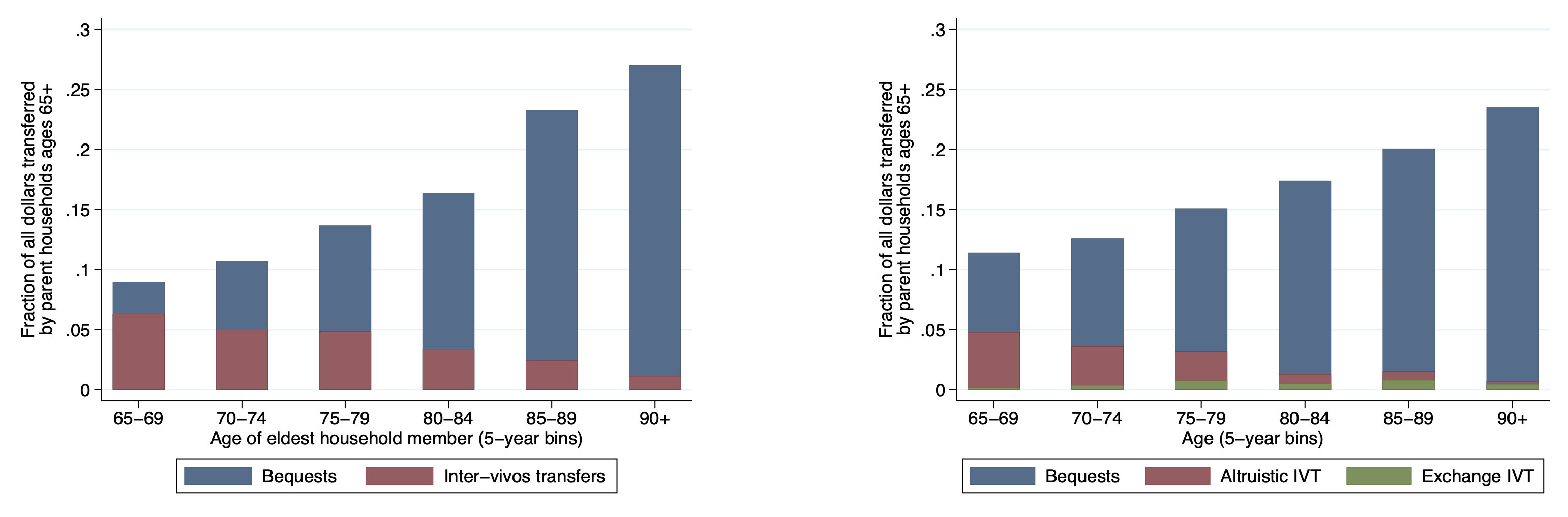

Finally, it is well-documented that elderly parents delay most transfers to children until death. As a summary measure, we calculate that the ratio of inter-vivos transfers to bequests for households above age 65 is 0.3; see Figure 1 for the precise timing in the data and how our model replicates it. Existing theories have been silent on the timing of transfers since they have merely assumed that all parent-child transfers flow as bequests. This is unsatisfactory on two fronts: First, there are substantial inter-vivos transfers in the data, and they flow in situations where children most need them. Second, parents can transfer their wealth to children before their death, but they (usually) choose not to. Here, our research agenda goes beyond the literature, providing a parsimonious theory that makes predictions for both inter-vivos transfers and bequests, offering potential solutions for the puzzles mentioned above. We now briefly describe this theory.

a) Data (HRS) b) Model

Figure 1: Timing of parent-child monetary transfers.

Source: Barczyk, Fahle & Kredler (2022). Panel a) is based on the U.S. Health and Retirement Survey, years 1998-2012.

Our approach draws on life-cycle models, game theory, bargaining theory, and modern computational tools to construct quantitative models of the family. In Barczyk & Kredler (2014a, 2014b), we have generalised the canonical single-agent life-cycle model of consumption-savings decisions to two agents who can give altruistically-motivated transfers to each other. Our subsequent work (Barczyk & Kredler, 2018) then used bargaining theory to model how parent and child reach a consensus on the informal-care decision in old age. The resulting model features a variety of within-family transfers. First, altruistically-motivated transfers (i.e., transfers without a quid pro quo); these flow in the form of monetary inter-vivos transfers, bequests and child caregiving. Second, exchange-motivated transfers: the child gives care to the parent in exchange for a monetary transfer in the present or a bequest in the future. Fitting our model to U.S. data, we find that an informal-care subsidy would be a welfare-improving policy in the U.S., as it would lead to a substantial decrease in Medicaid-financed nursing homes, which are very costly to the government.

In our most recent article, Barczyk, Fahle, and Kredler (2022), we claim that incorporating housing into this theory allows us to make headway on the above mentioned puzzles. The main takeaway is that interactions between old-age risks, family insurance, and housing are critical. In everyday language, our model tells the following story. Imagine a widower who contemplates whether to sell his house. He has few other financial assets but a decent Social Security pension. Selling his home would enable him to consume more. However, he figures that if he were to require care, having a house would make it more likely to receive care from his daughter. After all, he could offer his daughter to live in his home while she provides care and bequeath the house to her after his death, thus compensating her for the burden of caregiving. If the daughter would not provide care, he would have to sell his home to pay for a nursing home, and so less wealth would be left over for her. Thus, he keeps the house and commits to a lower consumption profile. Finally, he asks himself: Why not transfer ownership of the house to the daughter earlier, in exchange for a promise of future care? He decides against this option as he feels that he is putting himself in a vulnerable position. The daughter may decide at some point not to care for him any longer, in which case he would be forced to move into a low-quality nursing home.

Economically speaking, the novel mechanism in our theory is that a house can serve as a commitment device that enables the family to achieve more efficient savings, meaning that both parties, parent and child, could be better off if they were credibly committed to a savings plan. We term this mechanism the housing-as-commitment channel (HACC), which we explain in an illustrative model that complements the large-scale quantitative model. HACC consists of two central ingredients. First, parent wealth resembles a common-pool resource (the classic example for such a resource being fishing grounds): both agents derive benefits from it—the parent while alive and the child as the residual claimant after the parent’s death. As such, parental wealth is subject to overuse: The parent does not fully internalise the benefit of his savings to the child, which depresses savings below the social optimum. The second ingredient is that the housing asset acts as a trust, enabling the parent to commit to minimal savings, thus guaranteeing a bequest to the child.

The critical reader may now wonder: Is the economist’s cold approach, rooted in mathematical modelling, really able to capture the intricate interactions and complexities in real families? For example, what if there is a social norm that puts pressure on children to give care to their parents? The family economist, and we, would answer as follows: First, economic models can actually capture non-self-interested concerns when incorporating altruistic preferences, a point that is sometimes misrepresented in the public debate. Second, social norms exist and shape behaviour to some extent. However, economic forces also shape –and overturn– social norms, at least in the long run. For example, in Scandinavian countries, where informal caregiving by children is almost absent nowadays, family care was the norm a century ago. As economic circumstances change –especially as female labour-force participation increases– there is increasing pressure in society that challenges and ultimately changes the notion that a daughter giving care to her parent is “normal” behaviour. Family economics helps us to understand these economic forces and to make better policy recommendations for the decades to come.

References:

Daniel Barczyk, Sean Fahle & Matthias Kredler: ”Save, Spend or Give? A Model of Housing, Family Insurance, and Savings in Old Age”, Review of Economic Studies, forthcoming

Daniel Barczyk & Matthias Kredler: “Evaluating Long-Term Care Policy Options, Taking the Family Seriously”, Review of Economic Studies, 85(2), 2018: 766-809

Daniel Barczyk & Matthias Kredler: “Altruistically-Motivated Transfers under Uncertainty”, Quantitative Economics, 5(3), 2014: 705-749

Daniel Barczyk & Matthias Kredler: “A Dynamic Model of Altruistically-Motivated Transfers”, Review of Economic Dynamics, 17(2), 2014: 303-328

About the authors:

Daniel Barczyk is Associate Professor at the Economics Department of McGill University (Montreal). His research interests are in Macroeconomics, Family Economics and Public Finance.

https://danielbarczyk-research.mcgill.ca/Daniel_Barczyk.html

Matthias Kredler is Associate Professor at the Economics Department of Universidad Carlos III de Madrid. He works on Macroeconomics, Family Economics and Labor Markets.

https://sites.google.com/view/matthiaskredlershomepage